-Updated 11/23/25

We are living through the fastest labor disruption in modern history.

AI and robotics are eliminating or transforming jobs three times faster than economists predicted just a few years ago. In the first ten months of 2025 alone, American companies announced 1.1 million job cuts—65% more than the same period last year. Verizon, Amazon, Bosch, Accenture, Microsoft, and Ford have announced massive restructures tied directly to automation and AI adoption. The people getting hit hardest are 47-50 years old, at the exact moment most families are earning and saving the most for retirement.

The problem isn’t technology. The problem is that our current economic systems were never designed for this pace of change.

UBI, robot taxes, retraining grants—these are solutions built for a slower world. They redistribute the pain, not the progress. What we need now is a way for people to share directly in the productivity of the machines that are replacing them.

This essay introduces the concept of Stability Capitalism and the AI Dividend—a neutral, innovation-friendly model inspired by Alaska’s 40-year-old Permanent Fund (run by Republicans) and Finland’s world-leading State Pension Fund (VER). Instead of punishing companies for adopting automation, it ensures every U.S. citizen aged 18-66 in households earning $75,000 or less receives $3,000 per month, direct deposited. Current Social Security recipients keep 100% of their benefits—guaranteed for life.

Because the truth is simple:

If AI is powerful enough to replace us, it’s powerful enough to pay us.

The Cliff Has Arrived

We are already standing at the edge. In the first ten months of 2025, U.S. companies announced 1.1 million job cuts—a 65% surge from 2024. Amazon’s 14,000 corporate layoffs, Bosch’s 13,000 cuts, Accenture’s 11,000, and Microsoft’s 9,100 show that this is not a theoretical debate—it’s a structural shift already underway.

The unemployment rate has barely moved (up just 0.1%), but that number hides the truth: one in four of the jobless—1.8 million people—has been out of work for more than six months. When benefits run out, many simply stop being counted.

Rehiring is brutal. Only 40-50% of laid-off workers land at the same or higher wage; the rest take a 10-20% pay cut. And the people getting hit hardest are not twenty-somethings. They are 47-50 years old, the exact moment most families are earning and saving the most for retirement.

Workers aged 45 and older now make up 55-65% of all layoffs—a 45% increase from 2024. The Technology sector has been hit hardest, wiping out higher-paying jobs. Even stripping out government-shutdown noise, private-sector cuts are up 56%, with wage losses up 87% because the cuts are concentrated in higher-wage roles.

McKinsey, the World Economic Forum, and Oxford project 85-140 million U.S. jobs displaced by AI in the next decade. Manufacturing automation has already replaced millions of jobs worldwide since 2000, and the pace is accelerating.

Economists once believed this transition would stretch through the 2030s. Instead, the combination of generative AI, robotics, and algorithmic management has compressed a decade of change into three years.

This is not an anti-technology argument. It’s a pro-human one. Progress without distribution is collapse in disguise.

The Perfect Storm—Productivity Without People

Automation boosts output but channels its rewards to capital, not workers. From 2000 to 2024, the share of national income going to labor has fallen in nearly every major economy while profits have soared. A handful of individuals now control more wealth than ever in human history, while real median wages stagnate. The world has created its most productive generation of machines—and its most precarious generation of people.

If purchasing power collapses, even efficient markets stall. Every innovation cycle of the past two centuries—from the spinning jenny to the semiconductor—has eventually created new categories of work. But generative AI may be the first technology that produces value without proportionate labor demand. When the output of intelligence itself is automated, “retraining” entire populations becomes mathematically impossible.

We can’t take a 55-year-old data analyst, hand them a six-week course, and expect them to magically become a plumber. Meanwhile, they’ve already lost their job and are staring down the very real possibility of losing their home, their car, and their savings.

And let’s be honest: the high-paying white-collar jobs being automated away are not being replaced with equivalent roles. They’re being replaced with jobs that are lower-paying, physically demanding, and require years of hands-on experience, formal trade training, and state-specific certifications.

Take plumbing as an example. In many states, it takes 4-5 years of supervised work just to become a journeyman plumber—and 7-10 years to reach the top end of the field earning around $120K+. Apprentices typically start at $16-$24/hour, spend years in that stage, and then graduate to journeyman pay at $28-$38/hour. Only after years more in the industry do they qualify as a master plumber earning $40-$55/hour. And if they eventually own a small plumbing business, they might clear $150K-$250K+, but only if they manage overhead well and have enough techs working under them.

This is not a quick pivot. It is not a six-week transition plan. It is a years-long reinvention, and most displaced workers simply don’t have that kind of time, money, or physical capacity during an economic freefall.

There’s one more piece almost everyone leaves out of this conversation. We are heading into the largest retirement wave in U.S. history. A massive demographic shift is already underway: more people are exiting the workforce than entering it. With fewer workers, fewer high-paying jobs, and fewer taxable wages in the economy, we have to ask a hard question:

Where will the support come from to care for the disabled, the elderly, and the millions of people who rely on safety-net programs?

If our economic base shrinks while our dependent population grows, the math simply doesn’t work. Ignoring that reality won’t make the problem disappear.

Existing Responses — and Why They Fall Short

Governments and economists are not ignoring the problem; they are simply using the wrong tools for this phase of automation.

Universal Basic Income (UBI)—championed by Andrew Yang and the Basic Income Earth Network—would give every citizen a fixed stipend funded by general taxation. Its flaw is political and fiscal: it treats symptoms rather than causes and lacks any tie to the sources of machine productivity.

Robot Taxes, suggested by Bill Gates and trialed in South Korea, mimic payroll taxes for automated systems. They sound simple but discourage innovation and drive automation offshore.

Automation Adjustment Taxes (AAT) from MIT’s Daron Acemoglu or Brookings analysts aim to capture firms’ AI-related gains for retraining programs, but they are nearly impossible to measure consistently.

Data Dividends and training credits focus on digital platforms or reskilling grants, yet they remain piecemeal and temporary.

All share one limitation: they redistribute revenue after the fact instead of linking social benefit to the moment of value creation. They see automation as a problem to offset, not a shared asset to harness.

If AI is powerful enough to replace us, it’s powerful enough to pay us.

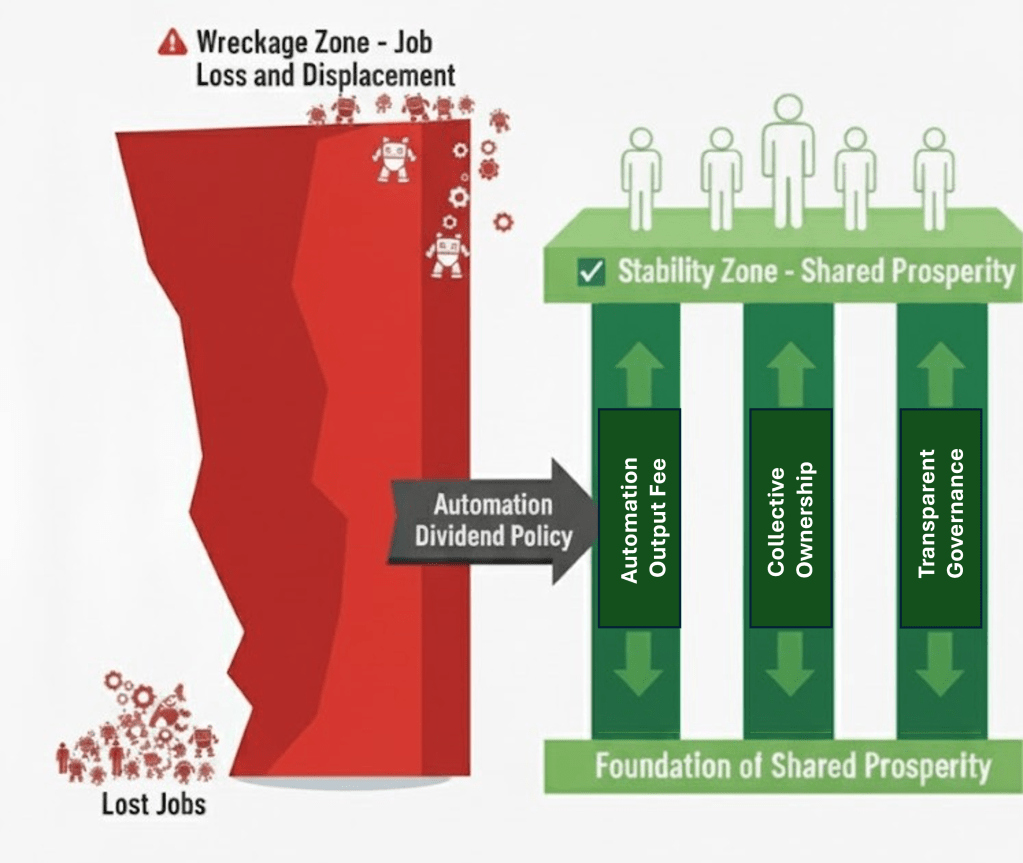

The AI Dividend Framework: Turning Automation into Shared Prosperity

If automation removes the human from production, it must also remove the barrier between citizens and the wealth it creates.

The AI Dividend does this through a simple mechanism: every U.S. citizen aged 18-66 in households earning $75,000 or less receives $3,000 per month, direct deposited—no apps, no tokens, no bureaucracy.

Current Social Security recipients keep 100% of their benefits, with automatic top-ups if they’re below $3,000/month. No senior ever receives less than an inflation-adjusted $3,000 per month—guaranteed for life.

The entire program is funded by a 0.054-cent fee on every commercial AI inference, collected at the U.S. cloud endpoint from Amazon, Microsoft, Google, OpenAI, and every other provider.

Zero new taxes. Zero deficit impact.

Cloud Endpoint Collection

The money comes from a 0.054-cent fee on commercial AI inferences—collected automatically at cloud endpoints (AWS, Azure, Google Cloud, OpenAI, Anthropic, xAI, etc.) every time a company uses AI compute. This is roughly 5.4 cents per $100 of corporate AI spend, less than one-twentieth of one percent of cloud providers’ gross margins.

The fee is baked into billing APIs, just like digital services taxes already are in 15+ countries. Cloud providers already track every millisecond of compute usage for billing purposes. Adding a dividend fee is a software update, not a revolution.

With 3.1 trillion inferences projected in 2026, that’s $1.62 trillion in revenue—enough to fund the entire dividend with surplus left over.

Why this works:

- No new taxes on individuals or small businesses

- Cannot be offshored (collected at the U.S. cloud endpoint)

- Automatically scales with AI adoption

- Politically neutral: It’s resource-sharing, not redistribution

The required infrastructure already exists. Cloud providers measure compute usage down to the millisecond, and transaction-level billing is routine across digital platforms. This isn’t a penalty; it’s a participation share. The more automation scales, the larger the shared pool becomes.

If Amazon Web Services can charge for a 300-millisecond inference, it can log a 0.054-cent Automation Dividend at the same time.

Direct Payment

The dividend hits your checking account the same way stimulus checks and Social Security do, direct deposit via the IRS and Social Security Administration infrastructure already in place. No blockchain wallets, no new technology, no friction.

If you can receive a tax refund, you can receive the AI Dividend.

No tokens. No wallets. No apps. No new bureaucracy.

Surplus Investment

Any surplus beyond the $1.62 trillion needed annually flows into a sovereign wealth fund modeled on Finland’s State Pension Fund (VER), which has averaged 8-9% real returns for decades. By 2040, this fund alone grows to $9-10 trillion—enough to replace Social Security and begin funding healthcare, forever.

The machines are coming for the jobs. We can let them take the country, or we can make them pay the rent and grow the dividend richer every year.

Who This Protects

Working-age Americans: $3,000/month base income for ages 18-66 in households earning ≤$75k

Current retirees: 100% of existing Social Security benefits protected—no cuts, no reductions, ever

People earning more: The dividend phases out smoothly between $75k-$110k household income; above that, you keep every dollar you earn with lower effective tax rates

This isn’t about replacing work—it’s about ensuring that when machines take jobs, machines pay the rent.

Learning from Alaska

Alaska has run a citizen dividend for over 40 years—funded by oil revenues, managed by Republicans, with zero inflation impact. Every resident receives an annual check from the Alaska Permanent Fund. It has broad bipartisan support because it’s framed as resource-sharing, not welfare.

The AI Dividend applies the same model to a different resource: artificial intelligence.

It is not welfare. It is the Alaska Permanent Fund Dividend (run by Republicans for 40 years), applied to the new resource: artificial intelligence.

Learning from Finland

Finland’s State Pension Fund (VER) offers the template for surplus management.

Founded in 1990 to prepare for future pension liabilities, VER invests across equities, fixed income, and infrastructure. It averages about 9% nominal (8.2% real) annual returns and operates with strict transparency and ethical screens.

Adaptation: The AI Dividend Fund

- Revenue Stream: A 0.054¢ fee on commercial AI inferences

- Fund Corpus: Globally diversified, ethically screened investments managed for long-term growth

- Payout Model: Monthly dividend to eligible citizens, while 96-97% of surplus capital stays invested

- Governance: Investment board, open-ledger reporting, stakeholder representation from government, industry, and labor

- Sustainability Rule: Withdraw no more than 3-4% annually—mirroring sovereign-wealth best practice—to maintain growth through downturns

We all share in the productivity of machines—they don’t replace us; they contribute to us.

Why It Works

Economically Sound – The fund grows automatically with automation’s reach; it doesn’t require new debt or distortionary taxes.

Politically Viable – Framed as profit-sharing, not punishment, it encourages innovation rather than stifling it. Republicans have run Alaska’s version for 40 years.

Technically Feasible – Cloud providers already measure compute use down to the millisecond; connecting those metrics to dividend distribution is achievable with existing infrastructure.

Socially Stabilizing – It keeps purchasing power in circulation and dignity intact. Displaced workers become shareholders in progress.

Population Growth Engine – $3,000/month removes money stress from fertility decisions. South Korea cash-transfer pilots (2023-2025) showed +18% birth-rate increases when women felt financially safe. U.S. births could rebound from 3.6 million (2025) to 4.2-4.4 million per year by 2035, fixing the Social Security worker-to-retiree ratio collapse.

Every structural change has trade-offs. The question is whether we design them—or let them happen to us.

Measurement – The fee is collected at the source: cloud endpoints track every inference for billing. No guesswork needed.

Governance – An independent Automation Trust overseen by multiple stakeholders—governments, civil-society groups, technologists, and labor representatives—prevents capture by any single interest.

Inflation and equity balance – Like Alaska’s oil fund, the dividend rises only when real output rises. That keeps incentives to innovate while protecting long-term purchasing power.

Housing inflation – The real worry is landlords capturing the dividend through rent hikes. The solution: companion policies including Land Value Tax (LVT), YIMBY zoning reform, and rent caps on empty units. These policies recapture 70%+ of rent-seeking while increasing housing supply.

Public understanding – When an AI system replaces 100 workers, those 100 should still share in its output. Framing it that way turns abstraction into fairness most people can grasp.

Implementation Roadmap

Pilot Phase (2026-2028)

- Choose three industries with high automation transparency

- Apply the inference fee and distribute dividends

- Publish results quarterly

National Scaling (2028-2030)

- Expand to all major automated sectors

- Create independent auditing bodies and public dashboards

- Interlink with international frameworks

Ideal: Global Fund Integration (post-2030)

- Merge national dividend pools into the Global AI Dividend Fund

- Standardize governance rules, ethics screens, and payout ratios

This timeline mirrors how carbon markets and pension funds matured: pilot → prove → federate.

The Bridge from Wreckage to Stability

Without action, RAND and the Congressional Budget Office estimate a cumulative $15-30 trillion loss to U.S. GDP by 2040 from collapsing demand, shrinking tax bases, and rising social instability.

History is unambiguous: when inequality accelerates this fast, societies either reform or fracture.

Stability Capitalism is the reform that works.

If we build it, automation becomes not a destroyer of livelihoods but a generator of collective wealth.

Fail, and the cliff only widens.

We built the machines. We can build the bridge—before the fall.

References

Acemoglu, D. & Johnson, S. (2023). Power and Progress.

Alaska Permanent Fund Corporation (2025). Annual Report 2025. https://apfc.org/annual-reports

Bureau of Labor Statistics (2025). Employment situation – September 2025 (USDL-25-1487). https://www.bls.gov/news.release/empsit.nr0.htm

Challenger, Gray & Christmas (2025). Layoff report – October 2025. https://www.challengergray.com/blog/2025-layoff-report-october

Congressional Budget Office (2025). The budget and economic outlook: 2025 to 2035. https://www.cbo.gov/publication/60870

McKinsey Global Institute (2025). The state of AI in 2025: Agents, innovation, and transformation. https://www.mckinsey.com/capabilities/mckinsey-digital/our-insights/the-state-of-ai-in-2025

OECD (2024). Who Will Be the Workers Most Affected by AI?

Oxford Martin School (2025). AI exposure predicts unemployment risk: A new approach to technology-driven job loss. PNAS Nexus, 4(4), pgaf107.

Pew Research Center (2025). AI risks, opportunities, regulation: Views of US public and AI experts. https://www.pewresearch.org/internet/2025/04/03/views-of-risks-opportunities-and-regulation-of-ai

RAND Corporation (2025). Macroeconomic implications of artificial intelligence (PE-A3888-3). https://www.rand.org/pubs/perspectives/PEA3888-3.html

State Pension Fund of Finland (VER) (2025). Annual Report 2025. https://www.ver.fi/en/annual-report-2025

Urban Institute (2025). The impact of AI on mid-career workers. https://www.urban.org/research/publication/impact-ai-mid-career-workers

World Economic Forum (2025). The future of jobs report 2025. https://www.weforum.org/publications/the-future-of-jobs-report-2025

For the full technical blueprint, economic modeling, and implementation details, read the complete Stability Capitalism white paper at ——

Leave a reply to rae43017 Cancel reply